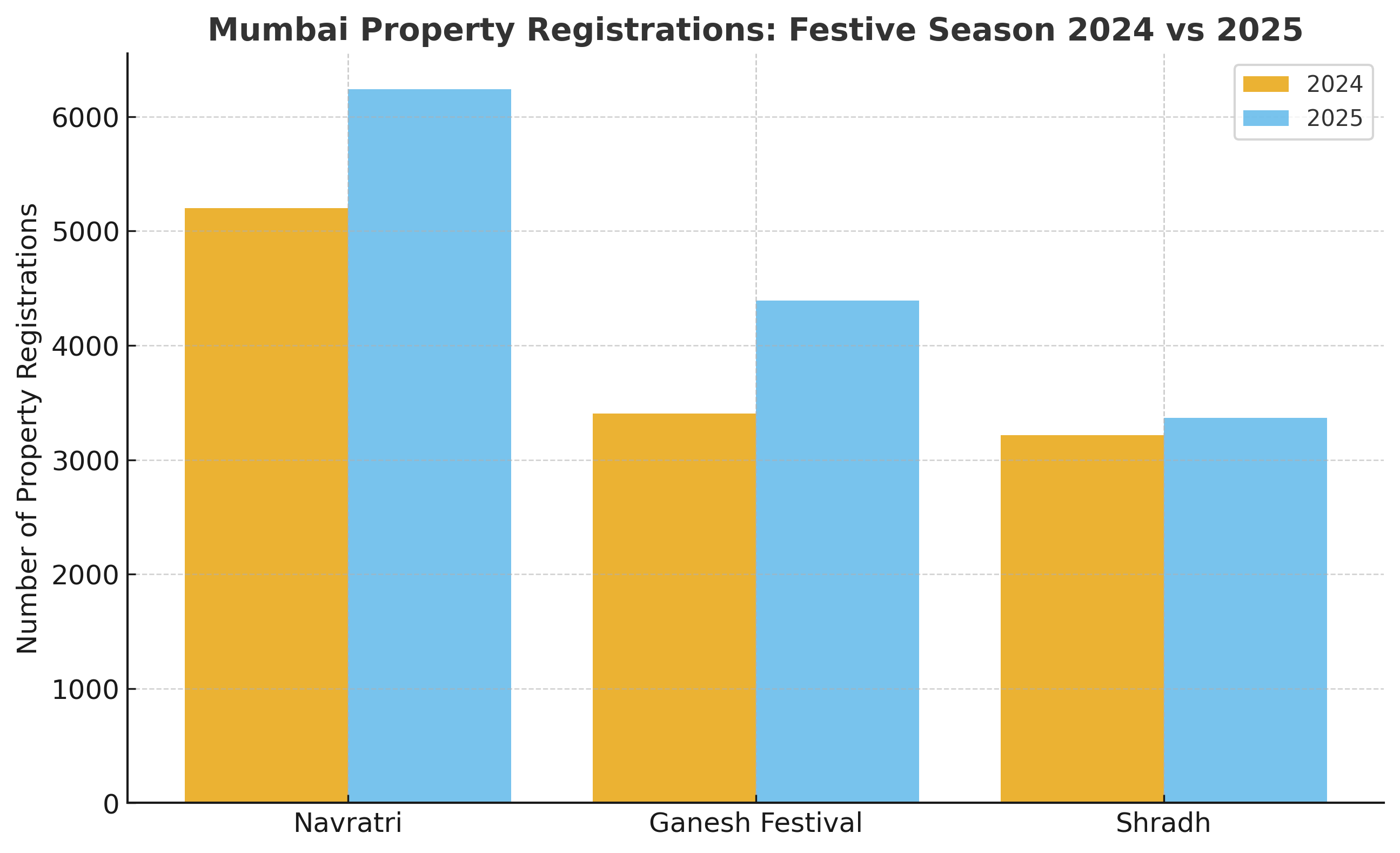

Traditionally, the holiday season brings happiness, lights, and a spike in sales. However, Mumbai's real estate market took off spectacularly in 2025. The city saw a 23% increase in property registrations during Navratri + Ganesh Chaturthi compared to the same period in 2024, with 10,630 registrations.

Even more remarkable is the 5% increase in registrations during Shradh, which is typically regarded as an unfavourable time for large purchases. Also browse latest Mumbai properties.

This blog breaks down the numbers, looks at the underlying patterns, identifies opportunities and risks, and provides strategic advice for realtors, developers, and buyers. To help readers process the main points, we'll also wrap up with a brief FAQ section.

Table of Contents

- Festive 2025 by the Numbers: A Snapshot

- Decoding the Drivers Behind the Surge

- Segmental Trends & Buyer Behavior

- Risks, Caveats & Sustainability Check

- What This Means for Stakeholders

- Conclusion

- FAQs

Festive 2025 by the Numbers: A Snapshot

Here’s what the data shows (based primarily on Maharashtra IGR data, analyzed by Knight Frank India) :

| Period / Festival | Registrations in 2025 | % Change YoY* | Notes / Additional Figures |

|---|

| Navratri (22 Sept – 1 Oct, 2025) | 6,238 | +20% | Compared to 5,199 in same span 2024 |

| Ganesh Festival (27 Aug – 6 Sept, 2025) | 4,392 | +29% | Compared to 3,405 in 2024 (27 Aug – 6 Sept) |

| Navratri + Ganesh Combined | 10,630 | +23% | Base: 8,604 in 2024 (same combined period) |

| Shradh (2025 vs 2024) | 3,368 vs 3,216 | +5% | Traditionally low period, now showing some resilience |

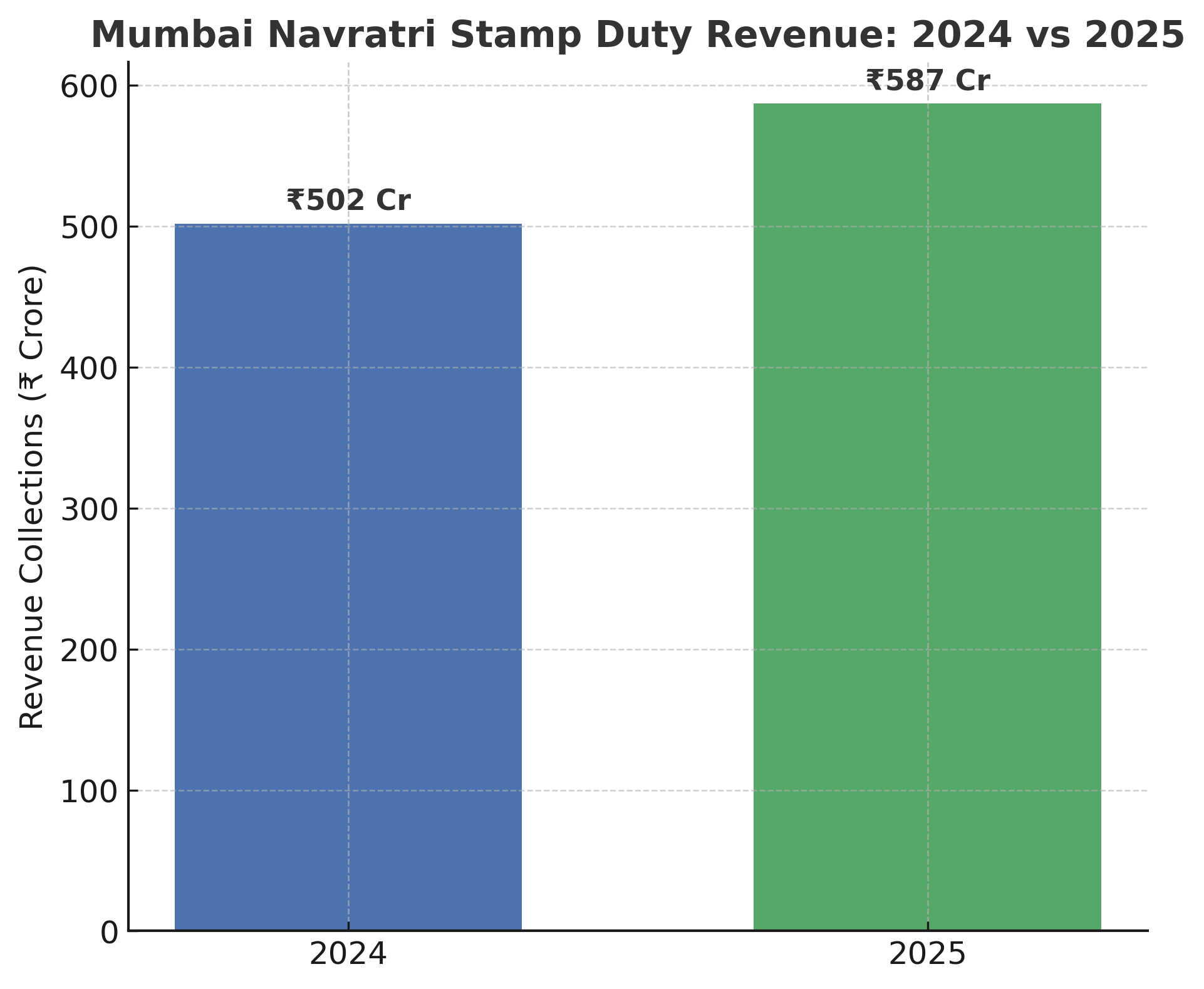

| State revenue (Navratri 10 days) | ₹587 crore | +17% | Versus ₹502 crore in 2024; average daily revenue up (₹59 cr/day vs ₹56 cr) |

* “YoY” = year-on-year comparison with the same period in 2024.

Another relevant context:

- The daily average registrations during Navratri increased from 578 units/day in 2024 to 624 units/day in 2025.

- The periods chosen for comparison are mostly time-aligned, though festival calendars can shift slightly, making perfect apples-to-apples comparisons tricky.

- In 2025, property registrations across Mumbai's municipal region for September leaped 32% YoY, and stamp duty collections jumped 47% in the same month.

-

- However, not all months saw uniform growth: in May 2025, property registrations fell ~4%, though stamp duty collections rose slightly, attributed to strength in the higher-value segment. If you are planning to purchase a dream home in Mumbai, then check current home loan rates in India.

-

Decoding the Drivers Behind the Surge

Numbers on their own tell a story — but the why behind them is more valuable. Below are key factors likely fueling the festive 2025 boom in Mumbai.

Festival Sentiment & Buyer Psychology

In India, purchasing property during festivals is considered auspicious. Developers and agents often roll out discounts, offers, and marketing blitzes targeting that belief. This cultural momentum can create clustering of buyer activity in fixed windows.

Even in traditionally inauspicious periods like Shradh, the increase (albeit modest at +5%) suggests that buyers are becoming more pragmatic and less bound by purely astrological guidelines.

Stable / Attractive Borrowing & Interest Rate Climate

One of the explanations cited by Knight Frank is that interest rates have remained stable (or favorable), making home loans more predictable.

When borrowing costs are stable, buyers feel more confident locking in deals, especially during periods when they expect some promotional pushes (festive offers) or easier negotiation.

Improving Affordability & Buyer Confidence

Affordability is a composite of income, interest cost, and price. If incomes are rising, inflation is under control, and the interest burden is acceptable, more buyers can enter the market. The article suggests that increasing buyer confidence has played a role.

In addition, simplifications or rationalisations in GST/tax/regulation have been mentioned as tailwinds.

Supply Timing & New Launches

Festive windows are prime windows for developers to time new launches, discount campaigns, or inventory clearances. If new projects are opened or schemes (zero stamp, easier EMI, downpayment assistance) are announced, demand may get pulled forward. The article does not give a detailed breakdown of new launches, but this is typically a factor.

Base Effect & Calendar Shifts

Because festival dates shift year to year, the exact span of days compared may include or exclude high- or low-volume days. For example, in September 2025, the Shradh period ended earlier, so Navratri fell inside the core month, aiding September’s month-on-month strength.

Also, if 2024 had weaker registrations in those same windows (for whatever reasons), then the base is easier to beat.

Premium / High-Value Deals Pulling Up Revenue

Even if volume growth is solid, if a larger share of deals comes from high-ticket properties, the revenue (stamp duty, etc.) will rise even faster. Mumbai's premium segment has been gaining traction in recent quarters (e.g., homes > ₹10 mn) in Knight Frank’s prior reports.

Thus, even if the number of units doesn’t skyrocket, the value per unit may drift higher.

Segmental Trends & Buyer Behavior

To make sense of which segments are driving growth and how buyer preferences may be shifting, let’s dig into adjacent data and plausible inferences.

Volume vs Value – Who’s Leading the Charge?

While the article focuses on registration counts (volume), the sharp increase in revenue (e.g., a 17% increase in stamp duty revenue in the Navratri window) suggests value is rising too.

In broader Knight Frank/industry data:

- Mumbai’s price growth in H1 2024 was ~4% YoY.

- In Q3 2024, the share of sales in the ₹10 million+ bracket jumped significantly, indicating demand at the premium end is strong.

So in 2025, it’s reasonable to surmise that the bulk of the revenue uptick is driven by mid- and premium deals.

Home Size & Affordability Segments

In the broader Mumbai context, smaller homes tend to dominate volume due to affordability constraints. For example, in September 2025, ~80% of registrations in Mumbai belonged to residential properties; many of those were smaller units.

Globally (in Mumbai’s data scenes), units under ~1,000 sq ft or in the 500–1,000 sq ft bracket tend to lead. In September 2025, that trend held.

Thus, while luxury properties may grab headlines, the volume base is anchored by compact and affordable-to-mid homes.

Geographic & Micro-Market Disparities

The article does not break down which suburbs or zones are contributing most to the surge. But Mumbai’s real estate behavior is deeply segmented:

- Core South Mumbai, Colaba, etc., are ultra-premium, with fewer units but high value.

- Western Suburbs (Andheri, Borivali, etc.) and Central Suburbs (Goregaon, Kurla, etc.) often see bulk demand for middle-income buyers.

- Peripheral areas or satellite towns may have more room for discounts or new launches.

A sharper analysis would require access to IGR/registration data by ward or precinct.

Buyer Profiles & Motivation

Likely buyer types active in this surge:

- End users/home buyers: Looking for primary homes, especially first-time buyers or upgraders, often sensitive to interest rates and affordability.

- Investors/speculators: Particularly in Mumbai, some buyers may treat property as a store of value—festive windows with offers and expected capital appreciation can attract them.

- Premium/luxury seekers: Upgrading buyers eyeing luxury offerings may get drawn in by new launches with high-end amenities or limited-edition offerings.

- NRI/out-of-state money: Mumbai often attracts capital from non-resident Indians or high-net-worth individuals from other states.

Because registration data aggregates all these, we can’t cleanly segment, but the revenue jump suggests participation from relatively higher-value deals.

Risks, Caveats & Sustainability Check

While the festive surge is exciting, prudent readers must keep a balanced view, assessing what could go wrong or what to watch out for:

Month-to-Month Volatility & Dependence on Festivals

Such surges are often lumpy and concentrated in short windows. If non-festive months (e.g. May 2025) are weak (as observed), the annual average may smooth out to more modest growth.

Thus, one must not overinterpret short-term highs as uniform growth.

Supply Constraints & Inventory Bottlenecks

Growth is limited by supply. If developers have limited ready inventory or land constraints persist, the pent-up demand could bottleneck.

Further, if new supply is skewed to premium or niche segments, bulk demand in affordable/mid segments may struggle.

Cancellations, Defaults, or Delays

In real estate, initial registrations are only one part of the story: actual closings, defaults, and payment dropouts can erode volume. Sometimes festival deals are booked impulsively and later cancelled.

Rising Input Costs & Construction Inflation

If material costs, labor, regulatory costs, or interest rates increase, margins may compress or prices may have to go up, which can deter new buyers.

Macro/Economic Headwinds

Any macro slowdown (e.g. in GDP, job growth, credit growth) could eventually dent buyer confidence. Real estate is sensitive to macro swings.

Data & Attribution Limitations

- Registration counts include both primary (new sales) and secondary (resales) markets. The article doesn’t segregate them.

- The article’s attribution (stable interest rates, regulatory simplifications) is plausible but not proven with hard causative data.

Therefore, the surge must be seen as promising but not bulletproof.

What This Means for Stakeholders

Each stakeholder group should read these trends through their own lens. Below is a breakdown of implications and strategic advice.

- For Home Buyers

- Festive windows remain ideal entry points: If you were planning to buy, festivals may still offer better negotiation levers.

- Don’t be swayed purely by volume trends: Focus on fundamentals—location, builder track record, construction quality, possession timeline.

- Watch out for hidden costs: Sometimes promotional offers come with trade-offs (floor rise, long possession periods).

- Lock interest rates smartly: If possible, secure home loan rates before potential hikes.

- For Developers & Builders

- Time your launches & marketing around festival windows: The data underscores that festival periods still correlate with buyer action.

- Prepare inventory & deliverability: Only those with availability will convert.

- Tailor offerings for the rising mid & premium segments: Focus not only on ultra-luxury but also on strong mid-tier products with good amenities.

- Manage pricing strategy: avoid overly aggressive discounts that erode margins; balance urgency with sustainability.

- For Real Estate Agents & Brokers

- Increase outreach ahead of festivals: Build a lead pipeline months ahead so you’re ready when the window opens.

- Educate buyers on process & documentation: that helps reduce dropouts and ensures smoother closures.

- Highlight value propositions: In festive seasons, buyers compare deals — emphasis on floor plans, amenities, and builder credibility matters.

- Choosing the right agent in Mumbai is also an important task.

- For Policy Makers & Government

- Revenue windfall: Higher stamp duty & registration collections (e.g., ₹587 cr in 10 days) boost state exchequer.

- Sustain regulatory clarity & ease of doing business: stability improves buyer and developer confidence.

- Monitor housing affordability & supply: Ensure interventions or incentives for mid/affordable housing if that segment lags.

- Data transparency: Release disaggregated registration data (by zone, price band) to help all stakeholders make informed decisions.

Frequently Asked Questions (FAQs)

Q1. Does a 23% increase in registrations mean prices have jumped 23%?

No. Registration counts measure volume (number of deals), not price. Prices may have risen, but the 23% growth mostly reflects higher transaction volumes, or more deals in premium segments.

Q2. Why did Shradh, an inauspicious period, see a 5% rise?

Buyers may be becoming more pragmatic—less bound by traditional beliefs—and more driven by household life-cycle needs, financial readiness, or opportunistic deals being available.

Q3. Are these registrations new sales or resale transactions?

The data includes both primary (new) and secondary (resale) transactions. The article does not segregate them.

Q4. Is this trend sustainable throughout the year?

Not necessarily. Other months (e.g. May 2025) have seen softness. The festive boost is real, but consistent momentum will depend on macro stability, supply, interest rates, and buyer confidence.

Q5. Which segments (affordable, mid, luxury) are driving growth?

While registration volume likely leans toward smaller/mid homes for affordability reasons, the sharper uptick in state revenue hints that a nontrivial share of deals are higher-ticket (mid to premium). Broader trends in Mumbai’s real estate suggest premium ticket sizes have been gaining share in recent quarters.

Q6. Should I wait for further growth before buying?

Waiting can be risky. Real estate markets are cyclical, and growth may plateau or slow. If you’ve found a credible builder, a property you like, and financial comfort, securing within a strong window (like festivals) may be wise.

Conclusion

Mumbai’s real estate market has delivered a robust festive-season performance in 2025. With 10,630 property registrations during the Navratri + Ganesh window (+23% YoY) and even 5% growth during Shradh, we see more than just a seasonal blip — we see a market with underlying strength.

Stability in interest rates, improving buyer confidence, and regulatory clarity appear to be contributing to this resurgence. But surging volumes alone do not tell the full story; value growth, supply dynamics, and sustainability will determine how durable this momentum is.

For buyers, developers, and agents, the message is clear: the festive window still matters, but success lies in preparation, credibility, and aligning with evolving demand. Monitor monthly trends, avoid overreliance on a single period, and focus on fundamentals.

Trending News In Real Estate